Your credit report is like a financial fingerprint, reflecting your creditworthiness and financial habits. A healthy credit portfolio is essential for securing loans, mortgages, and even potential job opportunities. Lenders use this report to assess your credit risk, determining whether you are a responsible borrower. To build and maintain a robust credit portfolio, you must […]

Category Archives: Building Credit

11

Mar

Mar

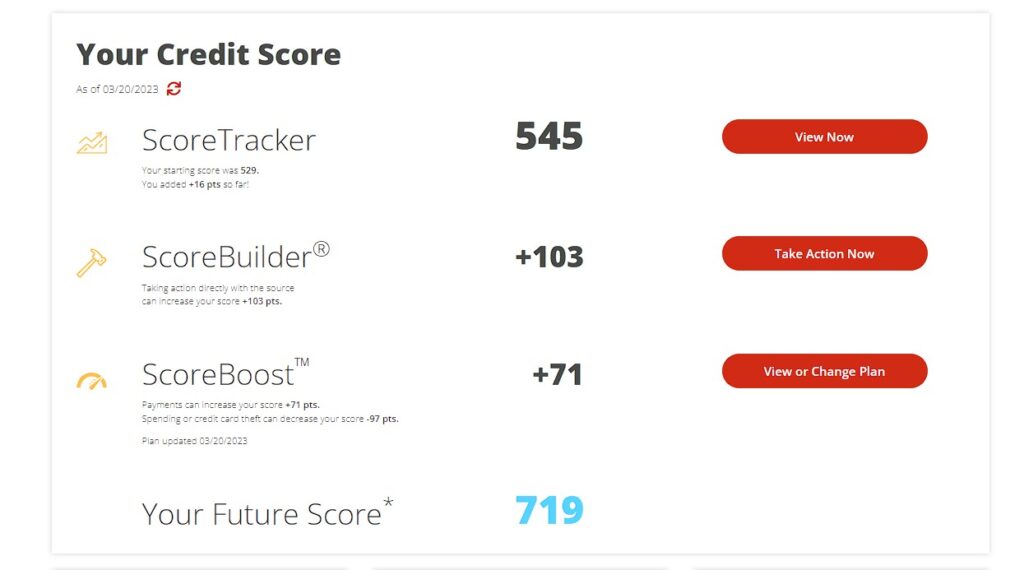

Building Up Your FICO When I graduated high school, like many students, I had no idea what a credit score was, how to build my credit or how big of a roll it would play as I progressed in life. Honestly, I thought to myself “If I can’t pay cash for something then and there, […]

15

Feb

Feb

Tools Of The Trade As my lease comes to an end and I think about the headache that is about to come when it comes to searching for another apartment, packing up all my belongings and moving into a new home; I look forward to the day that I can buy my own house. Currently, […]

13

Dec

Dec

Your credit report is like a financial fingerprint, reflecting your creditworthiness and financial habits. A healthy credit portfolio is essential for securing loans, mortgages, and even potential job opportunities. Lenders use this report to assess your credit risk, determining whether you are a responsible borrower. To build and maintain a robust credit portfolio, you must […]

24

Oct

Oct

Hello, my fellow financial enthusiasts! Today, I want to share a game-changing strategy with you that has brought me so much peace of mind when it comes to managing my credit card debt. It’s called the 15/3 Credit Card Payoff Method, and believe me, it’s a game-changer! Now, as we navigate the ups and downs […]

04

Aug

Aug

Your credit report is like a financial fingerprint, reflecting your creditworthiness and financial habits. A healthy credit portfolio is essential for securing loans, mortgages, and even potential job opportunities. Lenders use this report to assess your credit risk, determining whether you are a responsible borrower. To build and maintain a robust credit portfolio, you must […]

28

Mar

Mar

The In’s and Out’s of Refinancing In today’s blog, we will go over what it means to refinance, how to do it and when you should think about refinancing. Many homeowners refinance for a variety of reasons from combating ever changing rates to saving money on interest rates. What is refinancing? Refinancing happens when you […]

23

Mar

Mar

Tools Of The Trade As my lease comes to an end and I think about the headache that is about to come when it comes to searching for another apartment, packing up all my belongings and moving into a new home; I look forward to the day that I can buy my own house. Currently, […]

09

Mar

Mar

While credit repair can seem like a daunting task for many, Credit Armor allows consumers to quickly and easily dispute items on their credit report, negotiate debts and monitor their scores movement with just the click of a button. In some rare cases, after the disputes have been made and items have been removed from […]

06

Nov

Nov

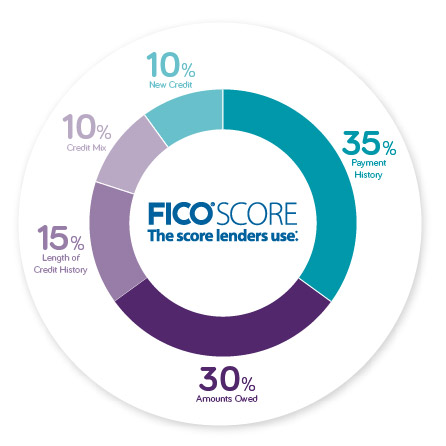

What comes to your mind when you hear the phrase “Credit Mix”. Most consumers imagine the credit pie chart that reveals the impact percentage of their payment history, credit length and utilization rates. Within the pie chart, there are two factors that make up 20% of your grade (new lines of credit and your […]

- 1

- 2