Score Tools & Features

Are you a Score Master, Builder or Protector?

Timing

Spending

Payments

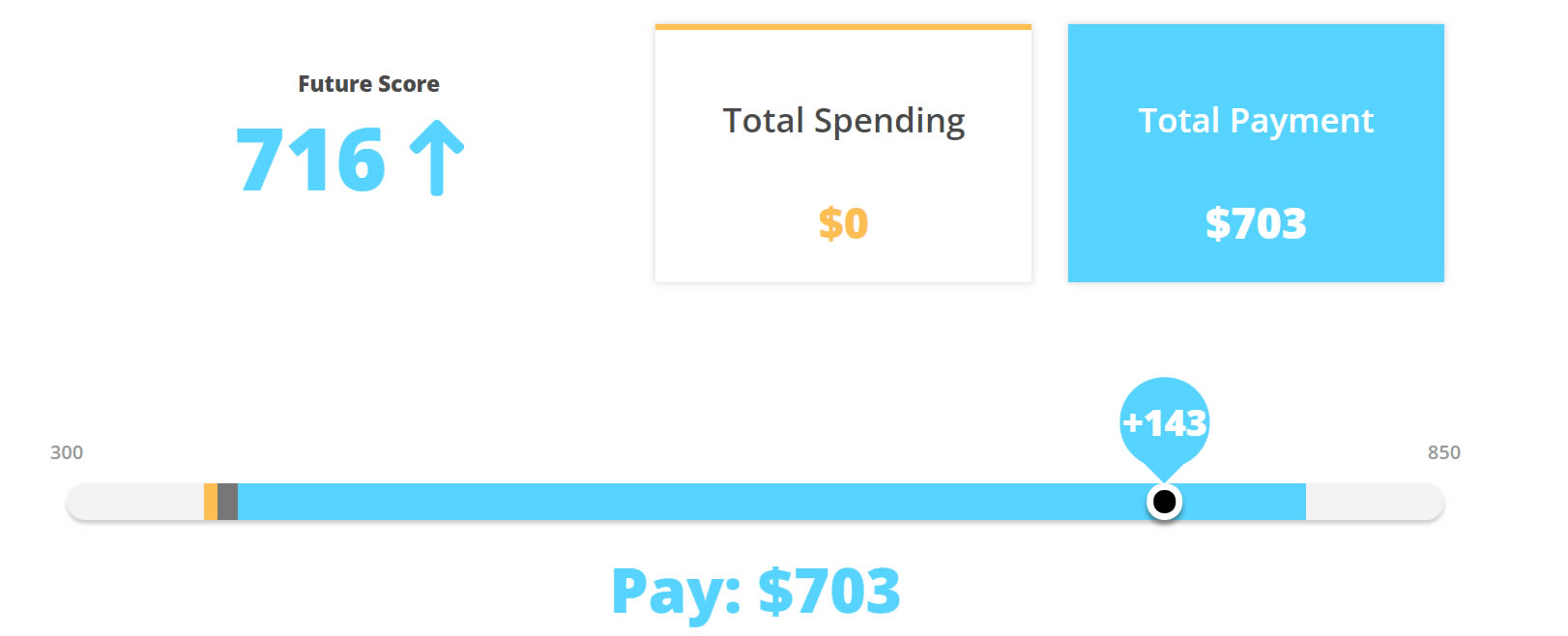

See how your payments can increase your credit score. Know how much to pay and by when.

Monitoring

We will actively monitor your credit cards and credit report to alert you of changes and detect fraud as your credit score changes.

Our ScoreBoost® is so easy to use! Just move the button to see what paying down your credit card or spending with your credit cards will do to your score.

Your Personal Plan

ScoreBuilder™ creates a personalized 120-day plan to help you understand what is hurting and helping your credit score, plus what actions you can take.

Take Action

Smart Connection

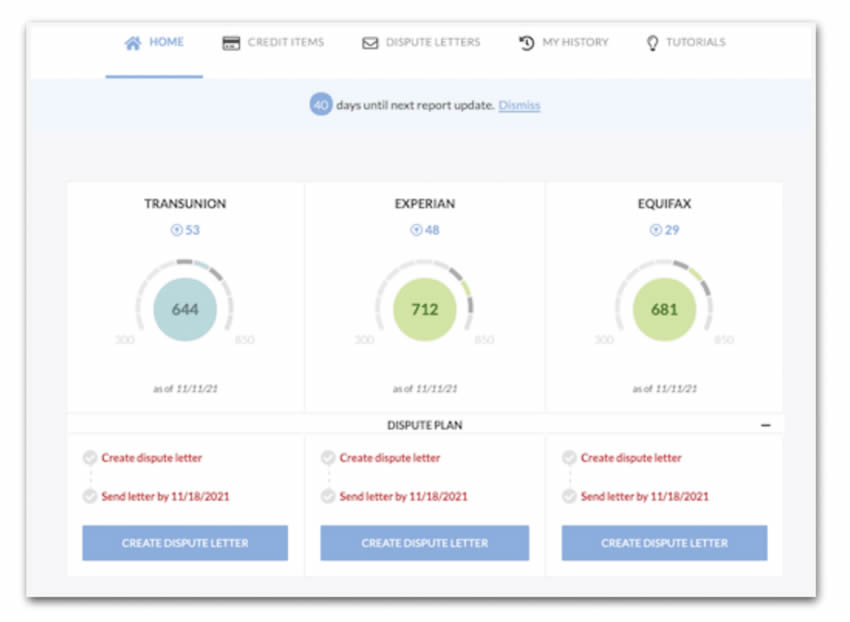

Create a strategy to help you remove negative items after you import and scan your 3 bureau credit report.

About ScoreTracker

Different Scores

Get an in-depth look at the different types of scores you have and see where you stand.

History

See how your scores change over time to get a better understanding.

Smart Credit Report®

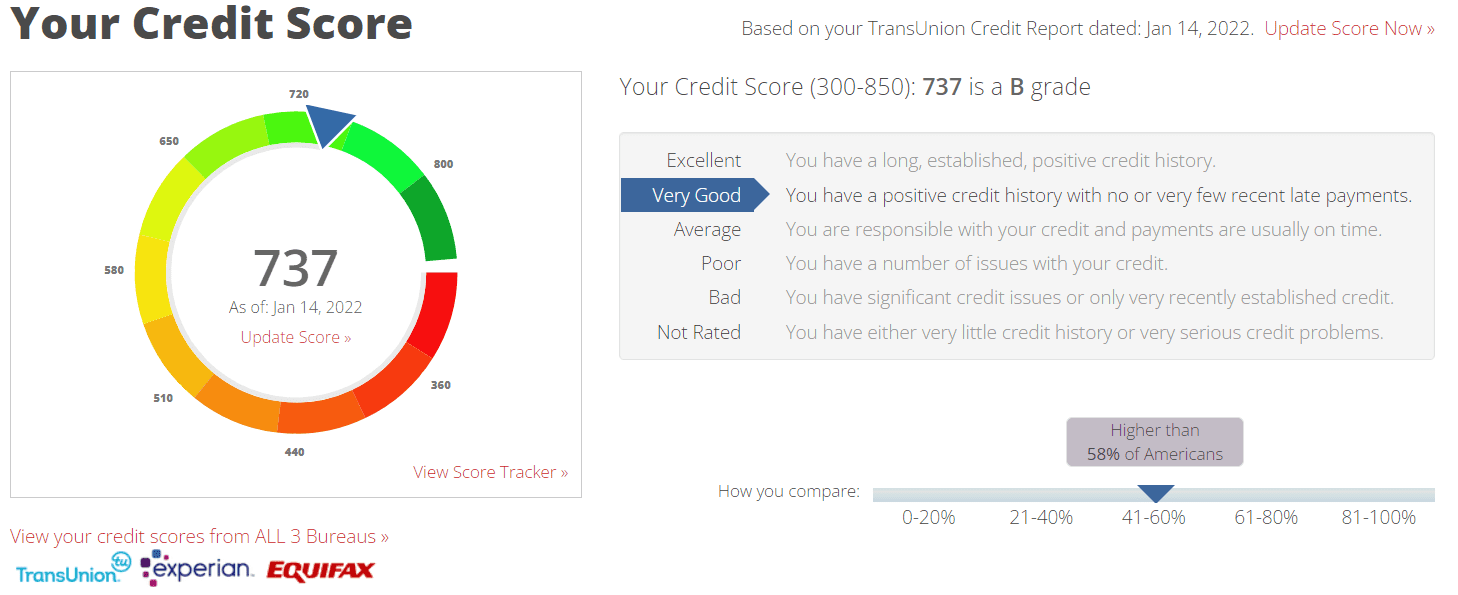

Credit Score

Your credit score ranges from 300 to 850 and is an overall view of your credit history, which is important to lenders.

Score Factors

Explanation:

A delinquency is a payment that was made 30 or more days late. You have had no or very few delinquencies recently which has caused your score to improve.

What You Can Do:

Keep paying bills on time every month since it is important for maintaining a good credit score. If you remain behind with any payments, bring them current as soon as possible, and then make future payments on time. Over time, this will have a positive impact on your score.

Explanation:

An installment account is one with a fixed monthly payment for the life of the loan. Auto loans and student loans are common examples of installment loans. Paying your bills on time improves your score. You have paid all your installment loans on time or no more than 30 days late.

What You Can Do:

Keep paying bills on time every month since it is important to maintaining a good credit score. If you remain behind with any payments, bring them current as soon as possible, and then make future payments on time.

Explanation:

Bankcard accounts include credit cards and charge cards from a bank and are frequently revolving accounts. Revolving accounts allow you to carry a balance and your monthly payment will vary, based on the amount of your balance. Your balances on bankcard or revolving accounts are not too high compared to the credit limit amounts, which causes your score to improve.

What You Can Do:

Keep low balances on your accounts; this will benefit your score.

Explanation:

Public records include information filed or recorded by local, state, federal or other government agencies that is available to the general public. The types of public records that can affect your score include legal judgments against you and tax liens levied by a government authority. You have few or no public records on your credit report, which increases your score.

What You Can Do:

Pay all bills on-time and satisfy all judgments. The impact that negative items such as public records have on your credit score will diminish over time.

Negative Score Factors: Explain Reasons Why Your Score isn’t Higher

Explanation:

Your oldest account is still too recent. A credit file containing older accounts will have a positive impact on your credit score because it demonstrates that you are experienced managing credit.

What You Can Do:

Don’t open more accounts than you actually need. Research shows that new accounts indicate greater risk. Your score will benefit as your accounts get older.

Explanation:

Bankcard accounts include credit cards and charge cards from a bank and are frequently revolving accounts. Revolving accounts allow you to carry a balance and your monthly payment will vary, based on the amount of your balance. The total combined amount you owe on all of your bankcards and revolving accounts is high, a sign of increased risk. People who carry balances on multiple bankcards or other revolving accounts have reduced available credit to use if needed, creating a greater chance of becoming overextended.

What You Can Do:

Pay down the balances on your accounts. Ideally, the balance on any revolving account should be 30% or less of the total credit limit on that account.

Explanation:

The balances on your accounts are high compared to the original loan amounts, lowering your score.

What You Can Do:

Paying down the balances on your accounts will benefit your score.

Your credit score is created using a mathematical formula that measures data from your credit report. Credit scores evaluate your payment behavior, debt levels and credit history. Factors like income, race and gender are not measured in the scoring process. Credit scoring systems are used by lenders, insurers, landlords, employers and utility companies to evaluate your credit behavior. Having a high credit score will help you receive the best rates on new credit and loans.

There are several factors taken into account that help determine your credit score. The factors making the largest impact are listed above. Remember that these factors vary in how strongly they impact your credit score. For example, if you have a very high credit score, the negative factors in your analysis are likely to have a small impact on your credit. For very low credit scores, the opposite is true in that negative factors have a very large impact on your credit.

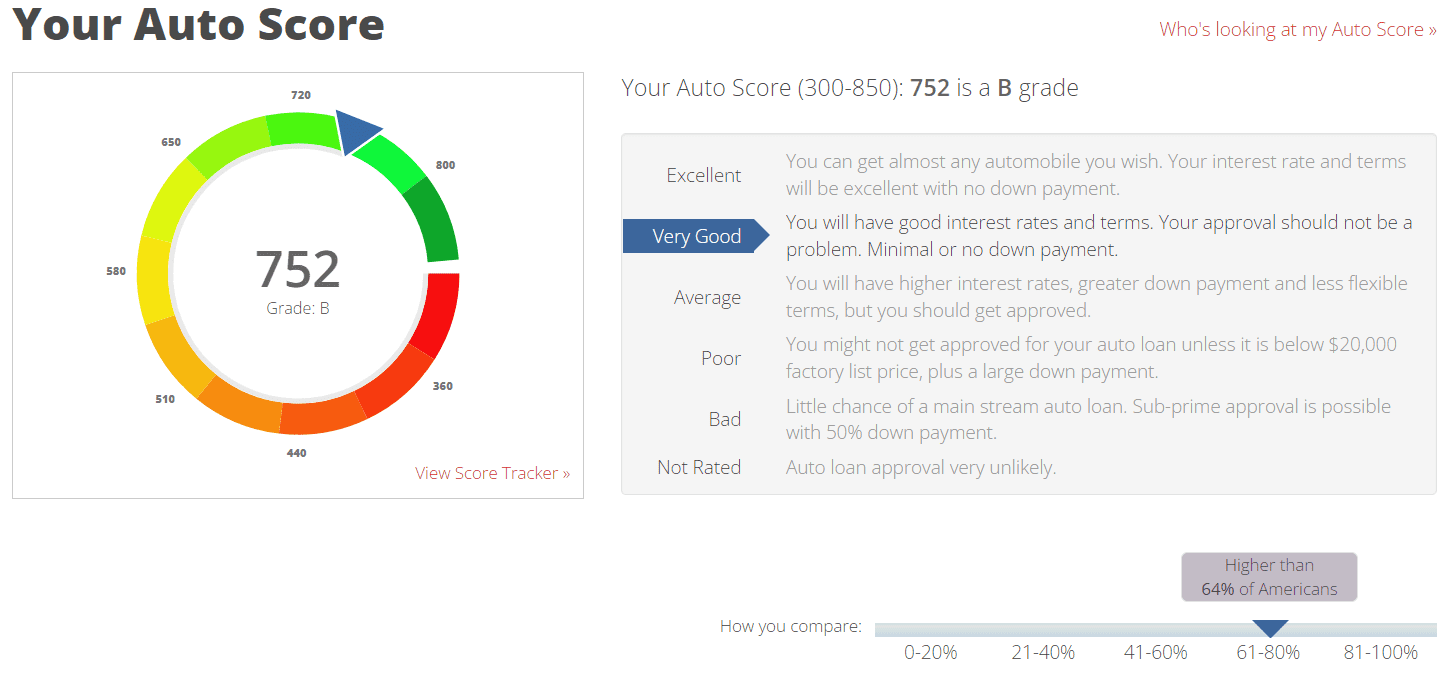

Auto Score

Auto lenders do not use your Credit Score. They use an Auto Score to better determine your lending risk.

What is my Auto Score?

This is your Auto Industry Optional Score used by those looking to determine your auto loan…. It is not very well known, but over 90% of all Auto lenders require this Auto Industry Optional Score to be used instead of your standard Credit Score.

The Auto Industry Optional Score is a specialized score that is used by the Auto Industry to look more closely at issues, on your credit report, that are related to your risk of possibly defaulting on your new auto loan. It is very different from your regular Credit Score.

HINT: When shopping for your new car, please know that most Auto dealers will ask you if you know your “credit score” when they are about to start your financing process. However, they will not tell you they are making their lending and financing decision based upon the much different scoring scale with their use of the Auto Industry Optional Score.

Generally, the Auto Industry Optional Score is not used on an on-going basis by your creditor to determine financial stress while your loan is still open. If it is the practice of your Auto lender to look at your credit while you have an open auto loan, they would most likely look at your regular credit score for the possibility of your sudden credit stress and risk of your defaulting on the auto loan.

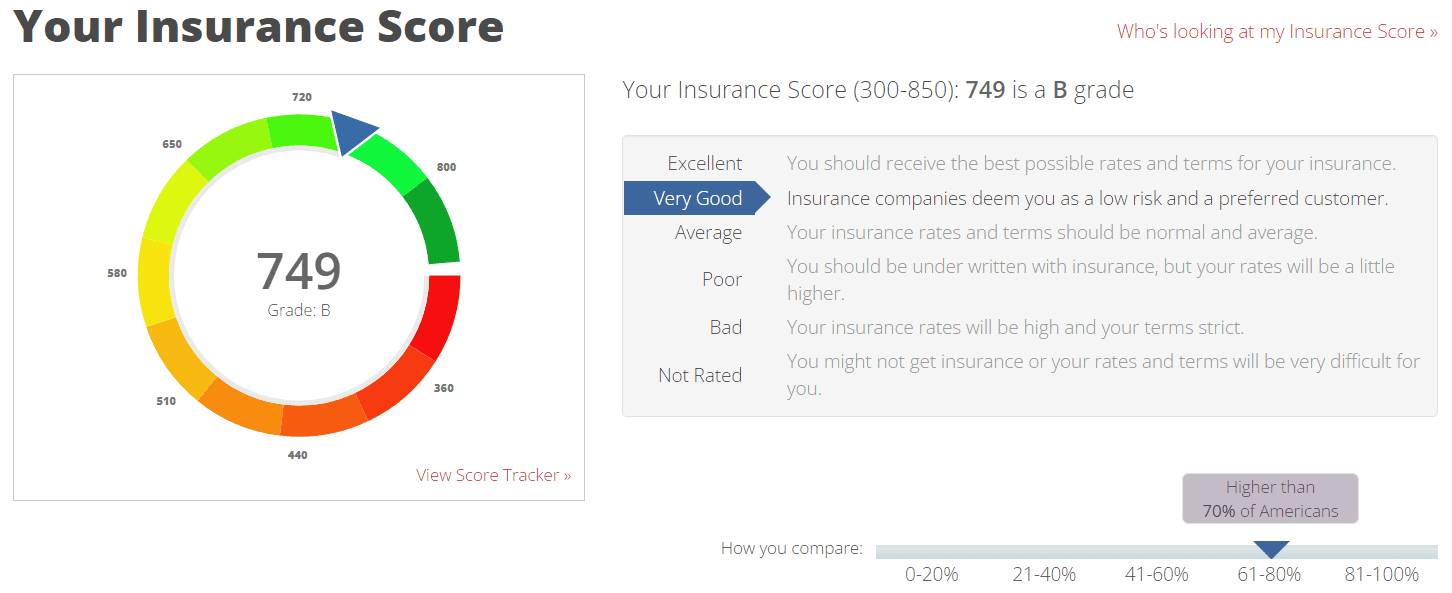

Insurance Score

This score is weighted to risk & stress factors most insurance companies use when looking at your credit.

What is my Insurance Score?

This is your Insurance Industry Risk Score. It is a highly specialized score… used by the Insurance industry to better understand your financial stress and find any prior defaults on insurance. This score is also used to determine if one has a propensity to make a fraudulent insurance claim due to current financial stresses.

This score is unique to the Insurance industry and might be used when you apply for any type of insurance. Generally, if this Insurance Industry Risk Score is not in your favor, it results in either higher premiums on your insurance or denial as permitted by applicable law.

This Insurance Industry Risk Score is generally not used to check on your credit status between your premium periods. For example, your Insurance company might only check this score once a year upon your renewal, or only at your initial application for insurance.

Any time you apply for Life insurance exceeding $150,000 the Insurer will check your credit and possibly use this Insurance Industry Risk Score to evaluate your overall risk and possibly deny you coverage as a result if your score is bad.

Some State laws do not permit insurance companies to use your credit to evaluate you.

Hiring Risk Index

What is my Hiring Risk Index?

This index considers many factors used by Employers in their hiring decision…, if they choose to look at your credit, as part of their hiring or employee promoting needs.

This is becoming more common. Currently, over 45% of Employers in the United States use your credit, in part, to determine the validity of your resume, your stability, verify your education (via a history of student loans) and your overall credit worth.

For most employment positions paying over $75,000 annually, prospective employers will check your credit.

It is very unusual for an Employer to check your credit during your employment, unless you are up for a promotion or you are a high-security employee. In any case, an Employer must get your prior permission in order to check your credit.

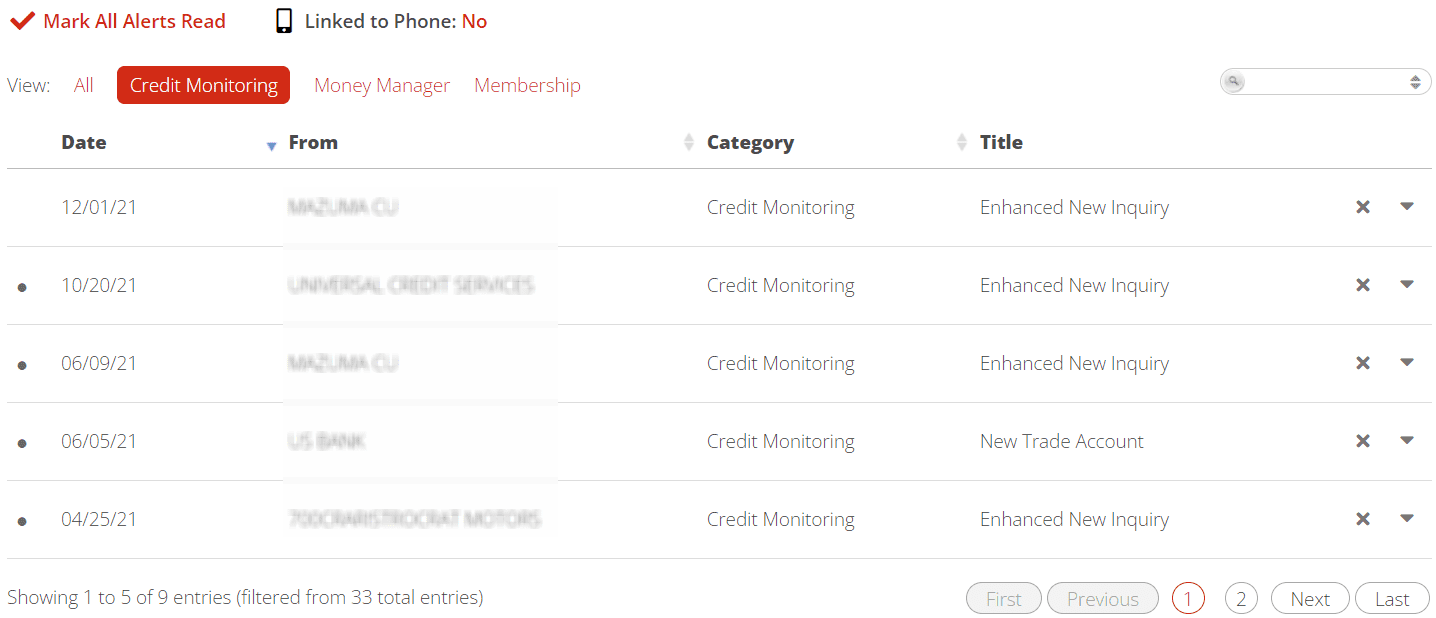

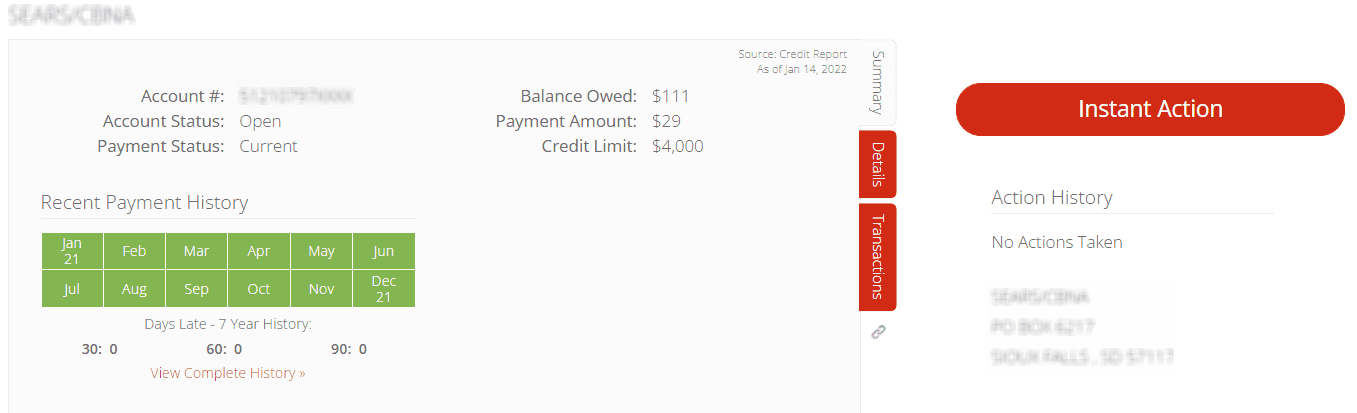

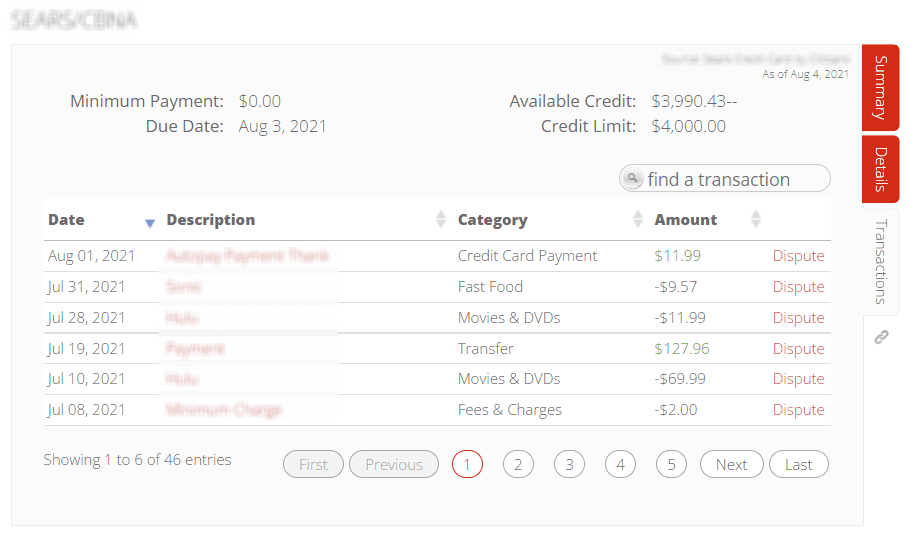

Credit Monitoring Alerts

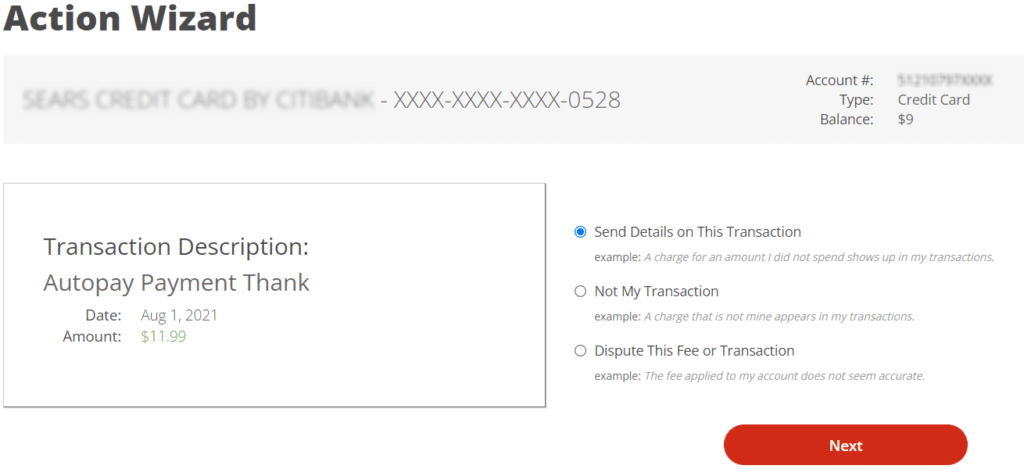

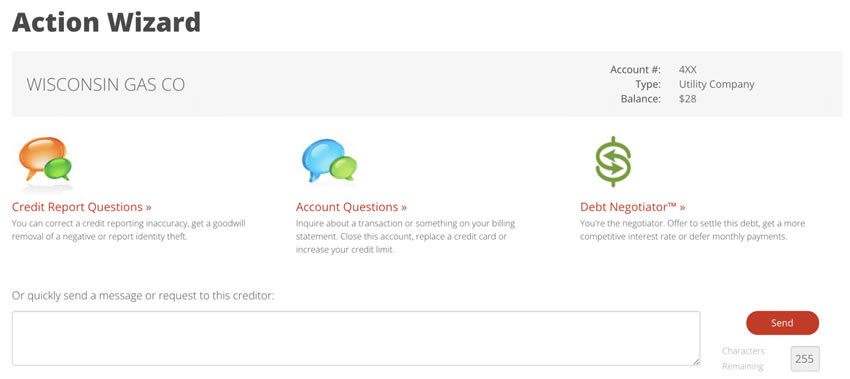

Use Action Buttons

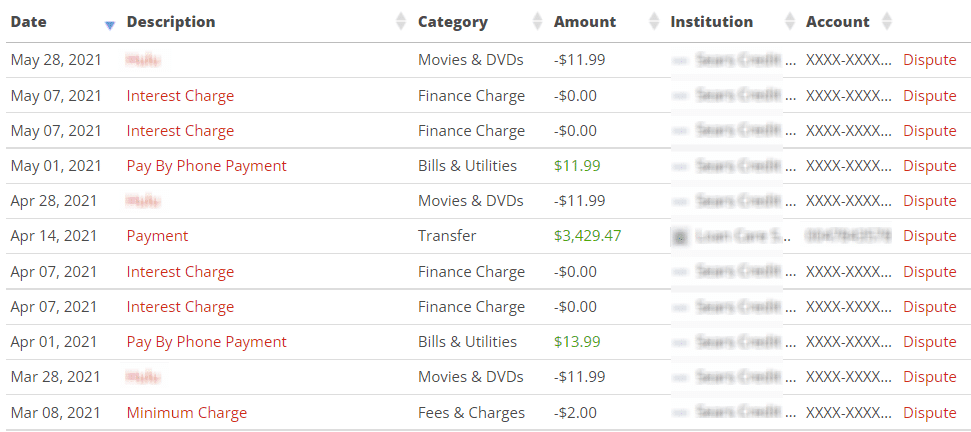

Daily Transaction

Dispute Armor

Fixing your own credit like an expert is now easy.

Dispute any account on all three bureaus

- Late Payments

- Repossessions

- Charge Offs

- Foreclosures

- Collections

- Judgments

- Inquiries

- Bankruptcy

Smart Connection

Brilliant Artificial Intelligence

Unlimited Disputes

Results & Follow Up

You can do this!

And we’re here if you need help.

Our software is so easy, tens of thousands of people have used it to fix their own credit.

You can too. We’re here for you.

Alerts & Insurance

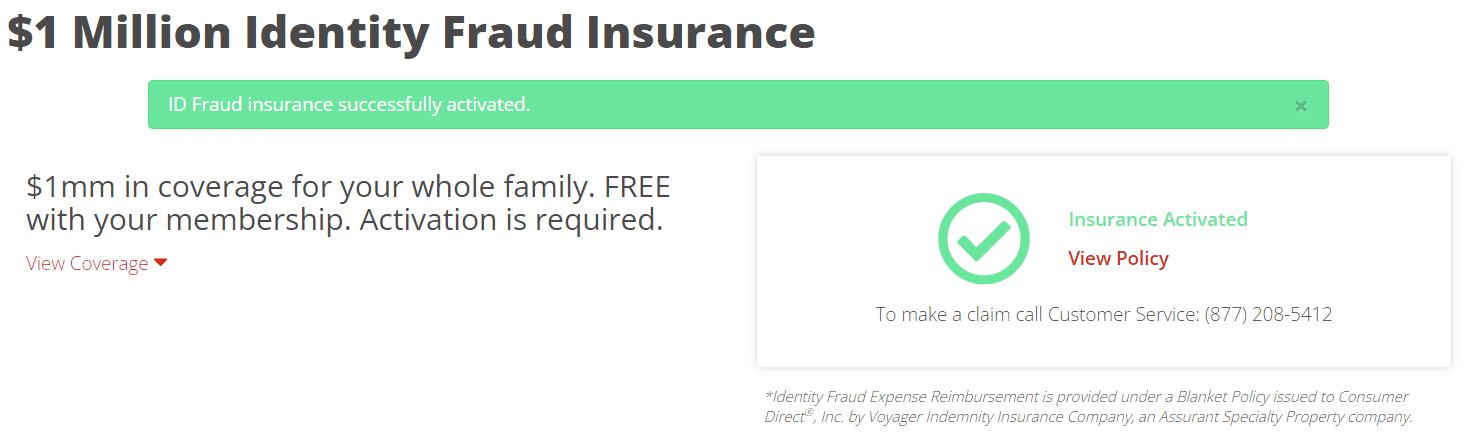

$1 Million Identity Fraud Insurance

*Activation Required

- Zero Deductible.

- Covers your entire family residing in your household.

- Covers your Bank, Savings, Brokerage, Lines of Credit, Credit Card, and more.

- Covers your cash out of pocket expenses incurred in your ID recovery.

- Covers your Credit Reports.

- Covers pre-existing Identity Fraud you didn’t know about.

- Replacement cost due to stolen Driver’s License or Passport.

What You Can Do With A Button

- Quickly inform your bank or creditor of an unauthorized transaction.

- Quickly respond to an unauthorized account activated in your name.

- No filling out lengthy police affidavits or forms.

- Avoid a lengthy bank or creditor process.

- No transfers to third party credit repair organizations.

- No lengthy phone calls or writing letters.

Money Manager

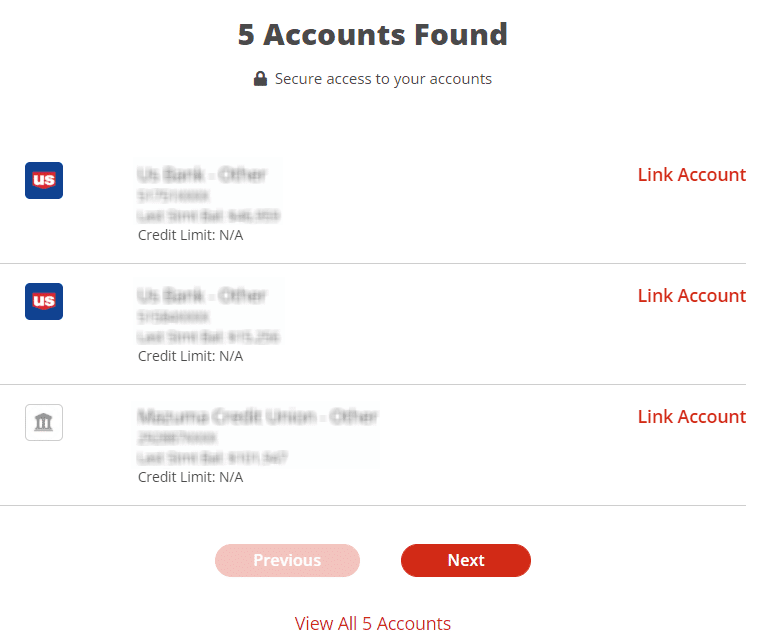

Our Action Buttons Connect You

We Find Your Accounts For You

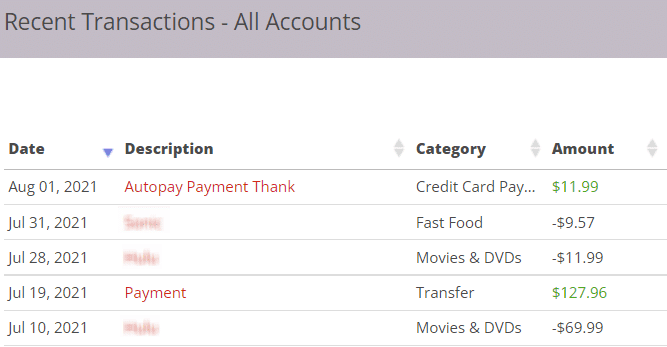

Daily Updates

Your transactions, instant statements, and trends are updated every 24 hours.

Transaction Monitoring Alerts have Action Buttons

Verify transactions are yours and not theft. Stop theft with the action button.

Easily Take Action

Ask your bank or credit card company anything with a click of a button.